The Pied-à-Terre Tax: New Rules, Exemptions, Appeal Deadlines and Penalties

On May 28, 2026, New York Governor Hochul signed into law a controversial and one of a kind “pied-à-terre tax” championed by the Mamdani administration that imposes a surcharge targeting non-resident luxury second homes that takes effect July 1, 2026, and is set to expire June 30, 2031, which is projected to raise fresh revenue to the tune of $500M annually.

This article will focus on the statute and regulations, its thresholds, two phase implementation, exemptions and potential penalties for non-compliance.

The legislature’s stated rationale for the law is that owners of luxury second homes benefit from city services without contributing proportionally. Critics note, however, that the tax arrives at a time when New York City is already losing high-net-worth residents to lower-tax jurisdictions. Moreover, the surcharge’s complex two-phase structure and aggressive compliance deadlines raise serious questions about administrability and fairness.

With the current ambiguity of the City’s regulations regarding valuation and applicable exemptions for covered properties, it is yet to be seen what amount will actually be collected on a year-to-year basis.

When Does the Surcharge Take Effect and How Is Value Determined? (Two-Phase Valuation)

New York City implements the pied-à-terre tax in two phases, each with different valuation methods and thresholds that determine which properties are subject to the surcharge.

Phase 1: July 1, 2026 – July 1, 2028

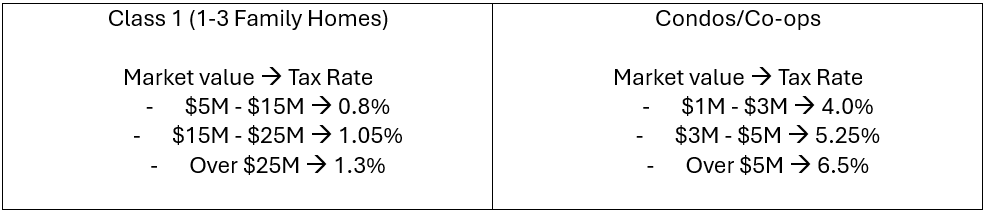

During Phase 1, the Department of Finance (the Department) values Class 1 properties (1–3 family homes) at market value as is typically determined under Real Property Tax Law § 581 and Real Property Law § 339-y, which is how local property taxes are currently calculated. For condominiums and cooperatives, the Department will use what is referred to as an “income-based valuation approach” which seemingly assesses these properties below local property tax values. Additionally, Phase 1 applies different market value thresholds by property type: Class 1 properties must have a market value of $5 million or more, while condos and co-ops must have a market value of $1 million or more.

Phase 2: (July 1, 2028- June 30, 2031)

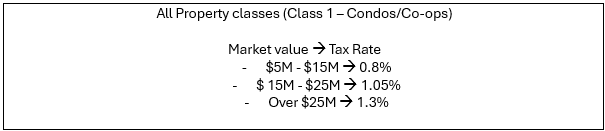

In Phase 2, the Department must value condominiums and cooperatives using comparable sales methodologies that disregard the valuation restrictions in Real Property Tax Law § 581 and Real Property Law § 339-y. This change is expected to significantly increase assessed values for these types of properties. Additionally, Phase 2 applies a uniform $5 million market value threshold to all property types and uses a single rate schedule (shown below).

The primary impact of the Phase 2 transition is on condominium and cooperative units, which are expected to see increased tax burdens as valuations shift closer to market value, while Class 1 properties are likely to experience comparatively minimal change.

What Qualifies as a Primary Residence?

A primary residence is one used as a primary residence, as of the taxable status date (January 5) immediately preceding the year in which the surcharge is imposed, by

- one or more of the covered owners[1];

- An immediate family member (a spouse, child, sibling, parent, grandparent, or grandchild) of one or more of the covered owners, provided such covered owners are natural persons;

- One or more lessees, and any sub-lessees provided any such lessee or sub-lessee is a natural person occupying such covered property or residential cooperative dwelling unit pursuant to a bona fide lease agreement negotiated in an arms-length transaction with a term of not less than one year.

Initial Determination

The Department will issue an annual “initial determination” to the covered owner as to whether the property is not a primary residence. The Department will make this determination based on factors that will be identified at a later date but will at least consider whether the property or residential cooperative dwelling unit was occupied in aggregate for a majority of days during a calendar year. Under NY Tax Law 1356 and Admin. Code § 11-3207, the Department may obtain this information pursuant to an information sharing framework between the City and State which may include NYS income tax returns. NY Tax Law 1352(a)(5) provides that the imposition of the tax is still valid even if the Department fails to issue the Initial Determination notice.

The Initial Determination can be rebutted by certifying the following:

- The covered owner provided the address of such covered property or residential cooperative dwelling unit as the covered owner’s permanent home address on the New York State resident income tax return filed for the calendar year immediately preceding the fiscal year in which the surcharge is imposed;

- Such covered property or residential cooperative dwelling unit received a STAR exemption or credit during the fiscal year immediately preceding the fiscal year in which the surcharge is imposed;

- The covered property or residential cooperative dwelling unit is the primary residence of one or more lessees or sub-lessees to which a lessee has sublet such covered property or residential cooperative dwelling unit or an immediate family member of a covered owner.

Notably, although Phase 1 applies higher surcharge rates to condos and co-ops (up to 6.5%), Phase 2 is expected to increase overall tax liability for these properties because the comparable sales valuation methodology is expected to produce higher assessed values, bringing more units above the $5 million threshold and subjecting them to the surcharge.

Final Determination

If the covered owner unsuccessfully rebuts the initial determination the initial determination made by the Department will become a Final Determination.

How to pay the surcharge

The surcharge will be added to the statement of account for the covered property and will be due and payable in the same manner as real property taxes. For residential cooperatives, the cooperative corporation will collect the surcharge from the tenant-stockholder whose shares represent the dwelling unit.

How and When to Appeal

The enacted law and proposed regulations create two distinct procedural avenues for challenging the surcharge. It is important to note that Section 11-3206 of the Administrative Code, the provision governing Tax Commission review of the surcharge, was enacted in 2026 specifically for the pied-à-terre tax. Unlike the traditional NYC property tax challenge process (which has decades of interpretive caselaw), this is an entirely new review mechanism without established precedent.

Path 1: Department Administrative Appeal (30 Days)

Under the proposed regulations (§ 62-06(b)), an owner may file an appeal of any initial determination that the property is not a primary residence no later than 30 days after the date that notice of such initial determination is transmitted. The appeal must be filed in writing through an electronic portal designated by the Department and must include a certification that the property is used as a primary residence along with supporting documentation (such as tax returns showing the property as the owner’s permanent home address, government-issued identification, or proof of a qualifying lease).

If the owner fails to file an appeal or provide proof of primary residence within the 30-day window, the initial determination becomes a final determination of the Department and the owner’s ability to challenge the primary residence determination at the Tax Commission will be significantly limited, except to the extent permitted under § 11-3206, including where a valuation challenge is raised simultaneously. If the owner does appeal and is denied, that denial constitutes a Final Determination that may then be challenged through the Tax Commission procedures described below.

Path 2: NYC Tax Commission Proceeding (Section 11-3206)

Separately, Administrative Code § 11-3206 permits an owner to apply to the NYC Tax Commission for correction of the surcharge during the time the books of annual records of market value are open for public inspection. An owner may challenge:

- The market value of the covered property, on grounds that the valuation is “excessive” (i.e., exceeds the full value of the property) or “unlawful” (e.g., the property is not subject to the surcharge, is outside NYC, or cannot be identified from the assessment roll);

- An Initial Determination that the property is not a primary residence, but only if the owner simultaneously challenges the market value of the property; and

- A Final Determination that the property is not a primary residence.

For the fiscal year beginning July 1, 2026, the filing period for Tax Commission applications begins on the date the notice of surcharge is issued and ends on the last date for filing for the fiscal year beginning July 1, 2027. In subsequent years, the filing window appears to follow the same schedule as the standard Tax Commission filing calendar: January 15 through March 1 for most properties, or March 15 for Class 1 properties.

Path 3: Judicial Review (Article 7 / SCAR)

Filing an application with the Tax Commission is an express statutory prerequisite to judicial review. An owner may then challenge a Final Determination by the Tax Commission in accordance with Title 1 of Article 7 of the Real Property Tax Law, on the same grounds available at the Tax Commission (excessive or unlawful valuation, or primary residence status). Such a proceeding must be commenced within the time specified by Section 166 of the NYC Charter generally before October 25 following the Tax Commission’s final determination.

Audit Risk and Penalties

The Department reserves the right to audit “any certification or documentation of primary residency” for six years, which is notably longer than the typical three-year statute of limitations for an income tax audit. The Department may impose penalties of up to 50% of the surcharge, after notice and a hearing, if the Department determines that the certification or documentation submitted contains inaccurate or misleading information that is material and was submitted either negligently or in bad faith. The 50% penalty may also be imposed in the case of a residential condo, which has been divided into more than three units, to avoid the surcharge and the owner of the property made the division in bad faith.

Proposed Rules

The Department of Finance has issued proposed regulations to implement the pied-à-terre surcharge and has scheduled a public hearing on July 9, 2026. While these rules are not yet final, they provide important insight into how the Department intends to administer and enforce the tax, particularly with respect to documentation requirements, procedural deadlines, and penalties. The most notable aspects of the proposed regulations include the following:

- Limited Timeframe to Appeal: As discussed above, the proposed regulations establish that a property owner has only 30 days from transmission of the Initial Determination notice to file an appeal with the Department. Failure to timely respond results in the Initial Determination becoming a Final Determination and significantly limits the owner’s ability to challenge the primary residence determination at the Tax Commission, except as otherwise permitted under § 11-3206 (including where a valuation challenge is raised simultaneously). This framework is particularly problematic in light of the provision that the surcharge remains valid even if the Department fails to provide the required notice as a missed or defective notice could impair a taxpayer’s ability to timely preserve their rights.

- Corporate ownership: To “prevent gamesmanship among owners of real property” the proposed regulations would require corporate entities to hold an undivided fee interest or all cooperative shares in a property to qualify for the primary residence exemption. This ensures that individuals controlling entities with only fractional ownership stakes cannot use those structures to claim the primary residence exemption.

- Proving Primary Residence: The regulations would require specific documentation to establish primary residence status, including tax returns, government identification, and corroborating records (e.g., utility bills or leases), and set forth what constitutes acceptable proof for family members, tenants, and entity ownership.

- Penalties: The regulations set out how penalties will be calculated based on the effect of inaccurate or misleading submissions. If a false submission results in no surcharge at all, a penalty of up to 50% of the applicable surcharge may be imposed. If a false submission results in a lower surcharge, a penalty of up to 300% of the shortfall may be imposed (capped at 50% of the applicable surcharge).

If you are a non-resident and own a second home in New York City that may be subject to this new pied-à-terre tax, it is critical that you act preemptively to determine your potential exposure, including whether planning opportunities exist to exempt your second home from this tax and to ensure that you are meeting the deadlines to challenge an Initial or Final Determination.

A competent state and local tax attorney can guide you through evaluating your options, and if necessary, aggressively prosecuting your Appeal of an inequitable or incorrect Initial or Final Determination.

This article was prepared with the assistance of Rahaf Atyieh, a summer associate at Cole Schotz.

_________________________________________________________________________________________

[1] A “covered owner” generally includes individuals who own the property directly or through entities such as trusts, partnerships, LLCs, or corporations.

As the law continues to evolve on these matters, please note that this article is current as of date and time of publication and may not reflect subsequent developments. The content and interpretation of the issues addressed herein is subject to change. Cole Schotz P.C. disclaims any and all liability with respect to actions taken or not taken based on any or all of the contents of this publication to the fullest extent permitted by law. This is for general informational purposes and does not constitute legal advice or create an attorney-client relationship. Do not act or refrain from acting upon the information contained in this publication without obtaining legal, financial and tax advice. For further information, please do not hesitate to reach out to your firm contact or to any of the attorneys listed in this publication. No aspect of this advertisement has been approved by the highest court in any state.

Join Our Mailing List

Stay up to date with the latest insights, events, and more