CrossCountry Challenges Court Order in Gallo Mortgage Fraud Case

CrossCountry Mortgage is seeking to intervene in Christopher Gallo’s criminal case tovacate a court order that blocked its arbitration claim. The company aims to recover a $2.1 million sign-on bonus, arguing the dispute is separate from Gallo’s criminal charges.

CrossCountry Mortgage (CCM) filed a motion last week as it seeks to intervene in the criminal case against former loan officer Christopher Gallo, and to vacate a November court order that blocked the company’s arbitration claim against the former employee.

National Mortgage News first reported the legal action.

According to the Dec. 3 filing, the Cleveland-based lender is asking the court to let it intervene to challenge the stay and allow the process from the American Arbitration Association (AAA) to move forward. CrossCountry’s lawyers also point to a recent Third Circuit Court of Appeals ruling that questions the government’s authority in seeking such an injunction.

Also in the motion, CrossCountry’s attorneys say the company paid Gallo a $2.1 million sign-on bonus in 2023 with a contractual agreement requiring repayment if he left the company within 36 months.

Gallo, who faces federal mortgage fraud charges, previously worked for NJ Lenders Corp., where he was a top producer. He and his assistant, Mehmet A. Elmas, were charged by the Department of Justice (DOJ) in April 2024 for falsifying loan documents from 2018 through late 2023.

In October 2024, Gallo and Elmas were indicted by a federal grand jury on one count of conspiracy to commit bank fraud, eight counts of bank fraud, eight counts of false statements to a financial institution and one count of aggravated identity theft.

Due to Gallo’s criminal charges, he was terminated by CrossCountry before the 36-month period.

“The termination was premised entirely on the presence of the allegations of fraud and Mr. Gallo’s indisputable arrest and criminal complaint against him,” CrossCountry’s filing states.

As a result, CrossCountry sent Gallo a letter demanding repayment of the sign-on bonus, which he has reportedly not complied with. CrossCountry filed for arbitration with the AAA to recover the funds and argues that the court lacked authority to stay the arbitration.

CrossCountry told HousingWire it does not comment on legal matters.

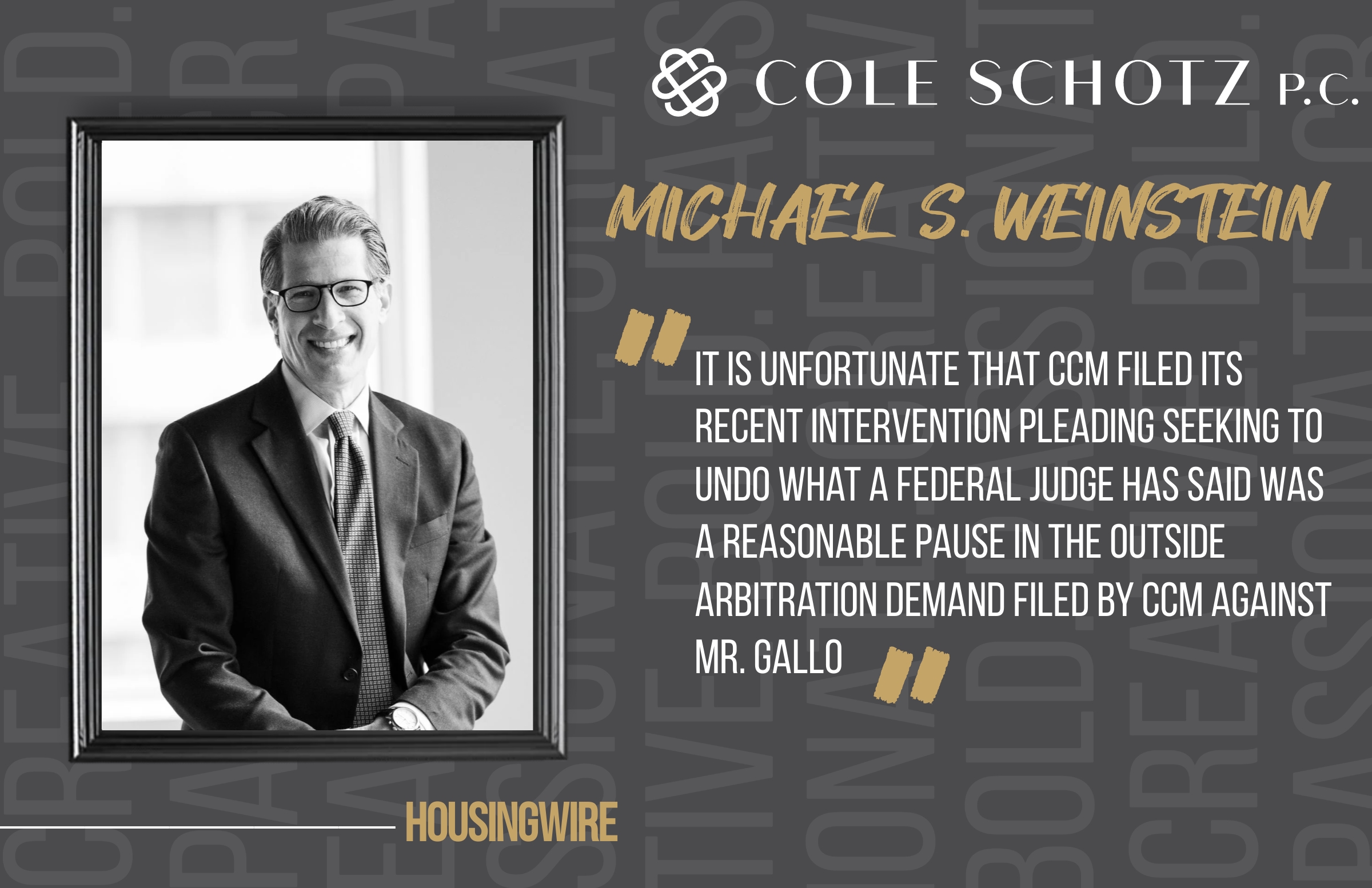

In an emailed statement, Gallo’s attorney, Michael S. Weinstein of Cole Schotz, called the filing “unfortunate.”

“It is unfortunate that CCM filed its recent Intervention pleading seeking to undo what a Federal Judge has said was a reasonable pause in the outside arbitration demand filed by CCM against Mr. Gallo,” Weinstein wrote.

“CCM’s Intervention filing is unique, and disfavored. Other Courts who, when examining this type of issue have ruled for a defendant and permitted him, rightly, to focus on the criminal proceedings as priority number one. Mr. Gallo will be filing a strong opposition this week.

“CCM waited 18 months to pursue potential claims against Mr. Gallo so the rush now to get that moving makes little sense,” he added. “CCM also seems to suggest that a defendant’s Constitutional Rights are not as important as the strictly financial claim they seek. I think they will find Federal Judges think quite differently.”

Gallo and the U.S. government jointly asked the court to block the arbitration, according to the filing. CrossCountry claims it was not copied on the letter and “was thus given no opportunity to respond or object to the requested stay.”

CrossCountry argues the dispute is simply about repayment of a bonus, not the criminal case, and should proceed under an agreement specifying arbitration in Ohio, where the company is headquartered.

If the motion succeeds, CrossCountry could move ahead with its $2.1 million bonus claim. If the stay remains, arbitration would be delayed until the criminal case wraps up, potentially pushing resolution into 2026.

As the law continues to evolve on these matters, please note that this article is current as of date and time of publication and may not reflect subsequent developments. The content and interpretation of the issues addressed herein is subject to change. Cole Schotz P.C. disclaims any and all liability with respect to actions taken or not taken based on any or all of the contents of this publication to the fullest extent permitted by law. This is for general informational purposes and does not constitute legal advice or create an attorney-client relationship. Do not act or refrain from acting upon the information contained in this publication without obtaining legal, financial and tax advice. For further information, please do not hesitate to reach out to your firm contact or to any of the attorneys listed in this publication. No aspect of this advertisement has been approved by the highest court in any state.

Related Articles

Join Our Mailing List

Stay up to date with the latest insights, events, and more